Compliance with credit card processing rules maximizes profits while mitigating risk. This is especially true for business to business companies. But it’s getting harder and harder with the onslaught of new rules, and virtually impossible if not using a sophisticated cloud solution to help manage compliance.

If your B2B company stores credit cards, there’s a pretty good chance you’re not compliant. For example, Visa’s 2017 Stored Credential Transaction framework outlines merchant responsibilities to obtain customer consent as well as storing credit cards, using stored credentials (token), and managing stored tokens. Failure to comply with Authorization rules, for example preauthorization and final settlement do not match, has far-reaching consequences including higher interchange rates (the bulk of credit card processing fees), penalty fees and new chargeback risks. With so many new rules across multiple card brands that vary based on business and transaction type how can a business quickly ascertain if they’re compliant?

Most processing details occur seamlessly behind the scenes so merchants have not had a simple way of knowing whether they’re compliant. Until now.

Quick tips to validate compliance:

Is a transaction receipt delivered to customer when a stored credit card credential (token) is created? Compliant answer is yes.

Is cardholder authentication with a zero dollar authorization or a purchase transaction performed at the time token is created? (A small charge is not an acceptable practice.) Compliant answer is yes.

Does the receipt include “RECURRING” or “REPEAT SALE” for token transactions? Compliant answer is yes.

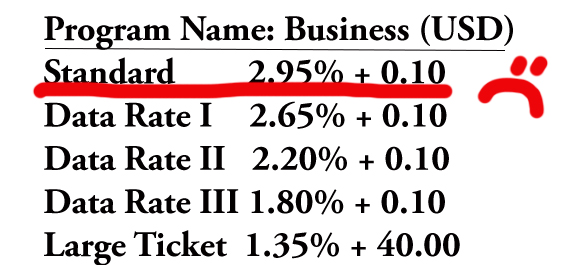

Review merchant statements, usually the last 1-2 pages with the heading “pending interchange” or “fees” section. Do you see EIRF, STANDARD (STD), or DATA RATE I? Compliant answer is no.

Can you produce documentation of customer consent to store their card (including with 3rd party service) and how it will be used?

If you’re not in compliance, your payment gateway is the most likely culprit, followed by ERP or other software integration limitation. For a Microsoft Dynamics AX, Dynamics 365, and other ERP integrated solutions, call 954-942-0483 9-5 ET.

Christine Speedy, CenPOS Sales 954-942-0483. CenPOS is a cloud business solutions provider with end-to-end payments engine that drives enterprise-class solutions for businesses, saving them time and money, while improving their customer engagement.

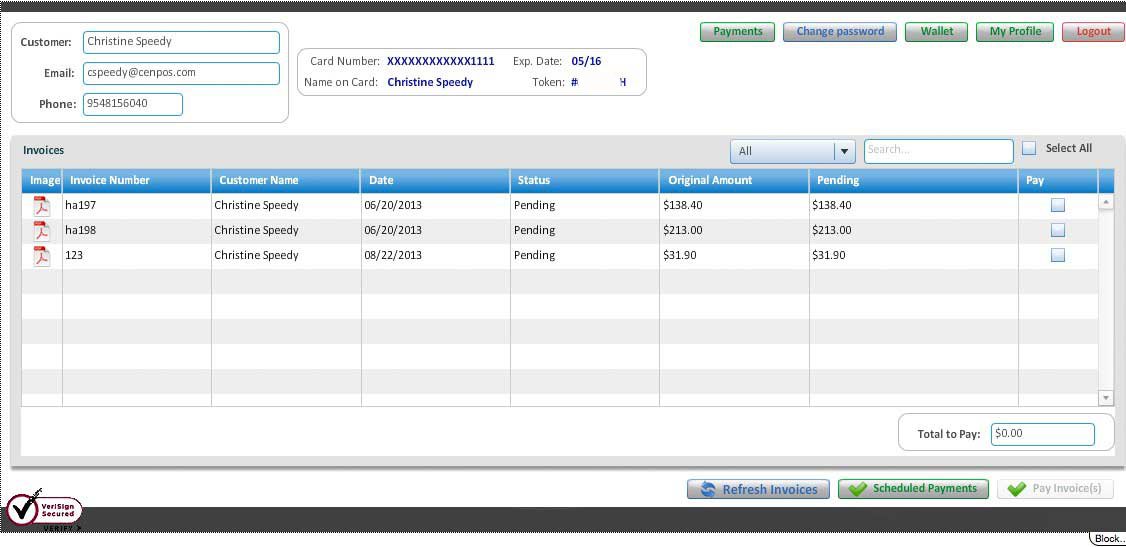

Yes, your customers can pay one invoice sent from an email without logging in to the invoice portal, or they can login and selected multiple invoices to pay. Our integrated payments module reduces customer friction to pay bills for Quickbooks Pro and Enterprise users and supports a variety of payment types and methods.

Note, you must have your own desktop or hosted version of Quickbooks. Quickbooks online does not support the ability to add 3rd party modules.

Quickbooks Merchant Services Vs CenPOS Payment Gateway & Platform:

Quickbooks Intuit Merchant Services nets fees from every transaction; CenPOS fees are charged once per month.

Intuit Merchant Services must use their acquirer. With CenPOS, choose any acquirer.

Quickbooks ACH nets their fees from every transaction. CenPOS fees are charged once per month.

Quickbooks sends monthly statements; CenPOS sends invoice reminders on your schedule with simple click to pay.

CenPOS supports level 3 processing and cardholder authentication to help you manage the cost of accepting credit cards and mitigate risk of chargebacks.

Christine Speedy, CenPOS business development 954-942-0483. CenPOS is a cloud based business solutions provider. Our cross-generational platform enables clients to expand their payment acceptance strategies, improve customer engagement, and increase business productivity.

Need a solution to process credit cards for Microsoft Dynamics AX 2012? Whether replacing Microsoft Dynamics ERP Payment Services due to end of life announcement, or looking for an alternative to Red Maple Advanced Credit Cards, Christine Speedy has a solution to delight your customers and make your business more profitable virtually overnight. It’s wrong to thing big name gateways are compliant with your B2B payment processing needs. If that were true, our solutions would not exist.

Dynamics AX Credit Card Processing Critical Features Checklist:

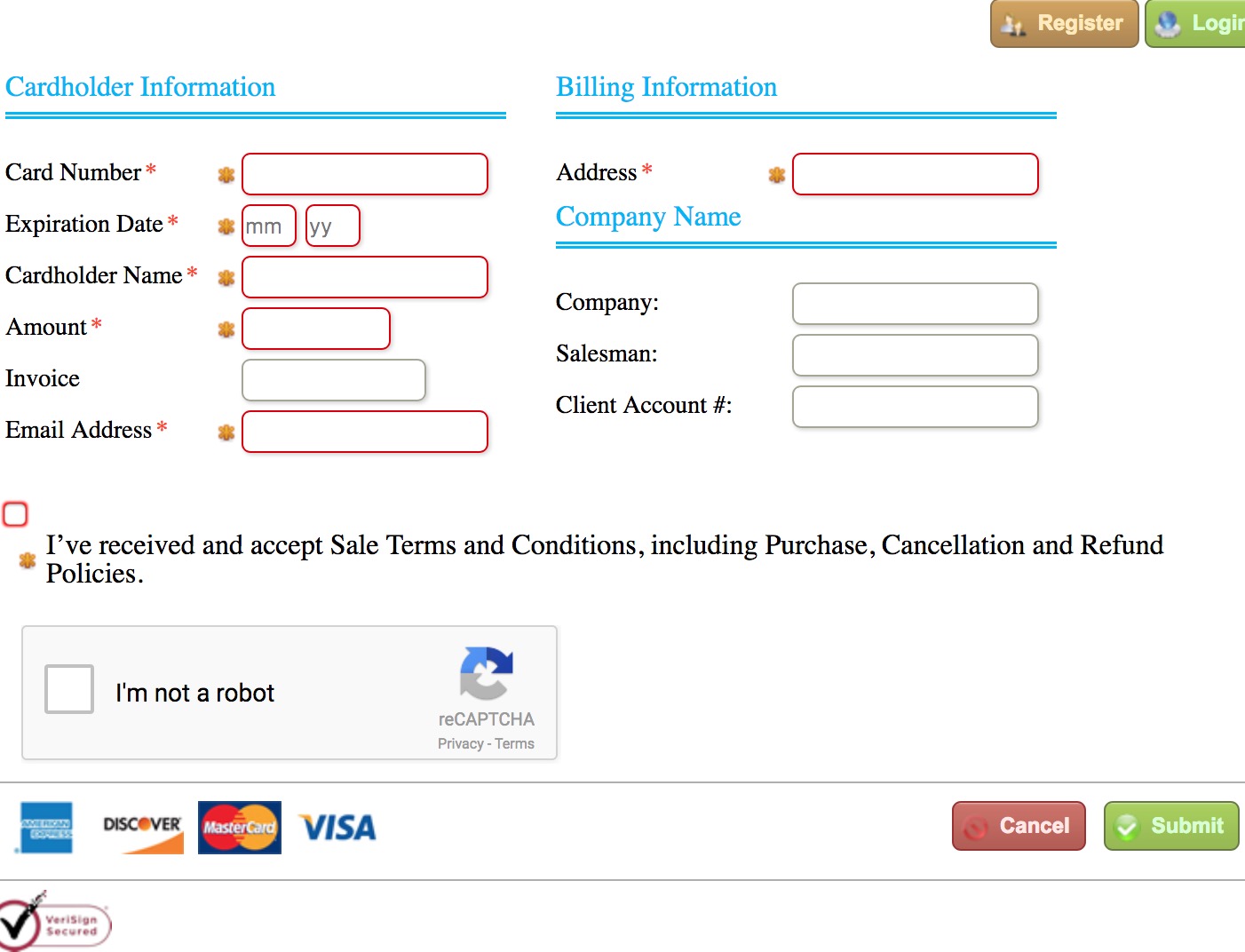

Customer managed wallet from the very first sale, including before payment is needed. Must eliminate need for paper or digital credit card authorization forms with card data in the clear!

No 3rd party applications needed to get paid from invoice; automate journal entry updates. (Eliminate BillTrust and similar.)

Communicate the way your customers want, both text and email.

Automate rate qualification. A payment gateway with Level 3 processing is not enough; merchants can only qualify for level 3 (corporate, purchasing, business card) interchange rates if all the rules are met. The two most common rules B2B businesses struggle with are “Settlement within 72 hours” for card not present sales, and “Authorization amount and settlement amount must be equal”. CenPOS automates compliance, most gateways cannot.

The same transaction can process at different rates, depending on which rules you follow.

Compliance with Visa Stored Credential Transaction framework and mandates effective October 14, 2017. Merchants need record of customers opt-in to storing and use of the stored card terms and conditions, among other items. For example, a checkbox. There are many nuances including identifying merchant initiated vs customer initiated. CenPOS automates compliance, most gateways cannot.

3-D Secure cardholder authentication- increase approvals, shift fraud liability risk, and for some card types qualify for reduced interchange rates.

Virtual Encrypted Keypad – segment your network, software and devices from payment processing for reduced PCI Compliance scope and burden.

Accept payments wherever you need in AX- free text, sales orders, payment journals and more.

Invoice portal – on demand access 24/7 to view and pay invoices

Automated collections reminders to pay

AX Solution for all payment types:

ACH and check, with and without guarantee.

Wire- eliminate inefficiencies matching deposits to invoices and returning unidentified wires.

Credit card

Paypal and more

Depending on your current AX set up, businesses can be live in less than 2 days.

Christine Speedy, CenPOS authorized reseller, 954-942-0483. B2B cloud payments solutions and CenPOS enterprise cloud payment solutions expert. CenPOS is a merchant-centric, end-to-end payments engine that drives enterprise-class solutions for businesses, saving them time and money, while improving their customer engagement. CenPOS secure, cloud-based solution optimizes acceptance for all payment types across multiple channels without disrupting the merchant’s banking relationships.

How can Magento developers help merchants get compliant with the Visa Stored Credential Transaction framework and mandates effective October 14, 2017?

Drive your profits while helping clients keep compliant with fast changing credit card processing rules.

Step by step guide:

How will clients manage consent record requirements? See Improving Authorization Management for Transactions with Stored Credentialshttps://usa.visa.com/dam/VCOM/global/support-legal/documents/stored-credential-transaction-framework-vbs-10-may-17.pdf . Will gateway provide a checkbox for consent records and ability to retrieve records on demand? (I called authorize.net on October 2 and they advised they will not offer this service, and will leave up to merchants.) Will you develop a custom application to include opt-in date, time and other requirements, plus storage and retrieval capability? Will you advise merchants to choose a technology solution, including payment gateway, that will manage automatically? CenPOS, a merchant-centric, end-to-end payments engine that drives enterprise-class solutions for businesses, saving them time and money, while improving their customer engagement will provide an automated solution for clients. Contact me for the plugin.

Update terms and conditions. Ensure online order terms include sale, refund and cancellation policies. Add a checkbox for customer opt-in to terms, including online payments. CenPOS has an opt-in box and you can customize the text.

Verify if there’s a system to manage authorization validity. What the heck does that mean? Many businesses, especially B2B companies, have complex needs including pre-authorizations, incremental authorizations, delayed shipping etc. While merchants may get issuer approvals, that doesn’t mean the authorization is valid. The two most common rules businesses struggle with are “Settlement within 72 hours” for card not present sales, and “Authorization amount and settlement amount must be equal”. (I asked authorize.net support about both items on October 2 and was told they do not offer automated solution.) CenPOS automates compliance. Other payment gateways are incapable or may leave it up to developers to create a solution. How can a developer verify if merchant has an issue? Ask clients to look at their merchant statement ‘pending interchange fees. If you see EIRF or STD, that’s a red flag there’s a problem.

Create a hosted pay page. B2B Businesses almost always have more than one sales channel and use of paper credit card authorization forms is common. They need help to eliminate. You already have the SSL certificate, so it’s a natural add on to provide clients a secure web page with an iframe a solution to collect payments. With CenPOS, end customers can use the same stored credential in Magento and the pay page, both credit card and ACH. Prevent brute force attacks. System hardening is a PCI compliance requirement. See Visa best practices to prevent brute force attacks. https://usa.visa.com/support/merchant/library/visa-merchant-business-news-digest.html. CenPOS includes recaptcha and client managed velocity and other rules as part of a layered security approach.

Payment Gateway checklist:

Verify payment gateway will send correct transaction data and flags for the initial transaction and subsequent transactions.

Advise clients to set gateway for zero dollar authorization when storing a new card.

Ensure client is registered for 3-D Secure and it’s enabled.

Confirm if gateway will automatically flag a transaction as customer initiated stored credential or merchant initiated stored credential (automated recurring billing). Additionally, the merchant initiated transaction must be sent with the MOTO indicator, not ecommerce.

Does gateway support level 3 data?

CenPOS manages all compliance and other items seamlessly in the background.

Communicate with clients. Advise any upcoming changes will increase efficiency and security for everyone. Advise clients to learn more about CenPOS payment gateway – call Christine Speedy, 954-815-6040.

Why comply? With full compliance and following my recommendations, merchants can expect better qualified interchange rates, increased approvals (avoid declines based on issuer risk averse algorithms), reduced PCI Compliance burden, fraud liability shift to issuer and increased efficiency for both buyer and seller. The cost of non-compliance is hefty, including higher interchange rates, penalty fees, and risk of both issuer and cardholder chargebacks.

The same transaction can process at different rates as shown above, depending on which rules you follow. CenPOS Smart Rate Selector automates compliance to qualify transactions at the lowest rate possible. Which rates are on your merchant statement now?

Magento developer billing: Developers also need to comply with recurring billing requirements for your sales. What’s worked before is not compliant- everyone needs to change.

DISCLAIMER: condensed and incomplete information! Information may be quickly outdated.

With the fast pace of changing rules, developers need a technology partner to automate compliance. Did you know?

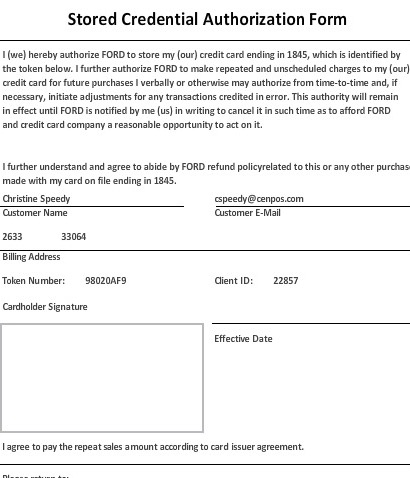

For those not ready to give up paper, CenPOS creates a printable PCI Compliant credit card authorization form for every stored card.

CenPOS has ERP, ecommerce shopping cart, accounting and other plug-in modules available for quick and easy implementation.

I’ve been selling for CenPOS since day 1. Though I have other payment gateways available in my arsenal, nothing else compares for meeting business to business needs.

Christine Speedy, CenPOS authorized reseller, 954-942-0483 is based out of South Florida and NY. CenPOS is a merchant-centric, end-to-end payments engine that drives enterprise-class solutions for businesses, saving them time and money, while improving their customer engagement. CenPOS secure, cloud-based solution optimizes acceptance for all payment types across multiple channels without disrupting the merchant’s banking relationships.

How can merchants get compliant with the Visa Stored Credential Transaction framework and mandates effective October 14, 2017?

Step by step getting started guide for B2B merchants:

Plan how you’ll comply with consent record requirements. See Improving Authorization Management for Transactions with Stored Credentialshttps://usa.visa.com/dam/VCOM/global/support-legal/documents/stored-credential-transaction-framework-vbs-10-may-17.pdf . Are you going to manage documenting everything or are you going to use technology to help you manage it? Ask your gateway if they’re going to provide a checkbox for consent and if you’ll be able to pull the opt-in records on demand. CenPOS, a merchant-centric, end-to-end payments engine that drives enterprise-class solutions for businesses, saving them time and money, while improving their customer engagement will automates multiple elements for clients.

Update workflow and documents. Ensure your sales order or associated credit documents include sale, refund and cancellation policies. Add a checkbox for customer opt-in to terms, including online payments. CenPOS has an opt-in box and you can customize the text.Verify if you have a system to manage authorization validity. What the heck does that mean? Many B2B companies have complex needs including pre-authorizations, incremental authorizations, delayed shipping etc. While you may get issuer approvals, that doesn’t mean the authorization is valid. The two most common rules B2B businesses struggle with are Settlement within timeframe for card not present sales, and Authorization amount and settlement amount must be equal. Per Visa Core Rules October 2017, for typical distributor and manufacturer card not present transactions, the authorization must settle no later than 7 calendar days from the date of the initial Approval Response. CenPOS automates compliance. Other payment gateways are incapable or may leave it up to developers to create a solution. Are you compliant now? Look at your merchant statement ‘pending interchange fees. If you see EIRF or STD, that’s a red flag there’s a problem.

Replace paper credit card authorization forms, and any digital form that you can decrypt and view sensitive card data. Offer your customers a way to self-manage their own wallet with either a hosted online pay page or Electronic Bill Presentment & Payment. CenPOS offers both options, including a lite ‘request a payment’ option, and lets your customers choose both text and email. For those not ready to give up paper, CenPOS creates a printable PCI Compliant credit card authorization form for every stored card.

New to online payments? See Visa best practices to prevent brute force attacks. https://usa.visa.com/support/merchant/library/visa-merchant-business-news-digest.html. CenPOS includes recaptcha and client managed velocity and other rules as part of a layered security approach.

Verify your gateway is ready or will be ready to send correct transaction data for the initial transaction and subsequent transactions for both customer initiated and merchant initiated use of the stored credential. You’ll want the payment gateway to perform a zero dollar authorization and authenticate the cardholder with 3-D Secure. Ask your gateway if it will automatically flag a transaction as customer initiated stored credential or merchant initiated stored credential, or if they’ll require you to have multiple gateway accounts, one for each type. CenPOS does all this for you now in a single account.

Get an ecommerce merchant account. This is needed for online payments. Don’t run mail order telephone order (MOTO) transactions on the ecommerce account unless you know your payment gateway can alter the flag sent with transaction to change the transaction type. Many cannot. CenPOS manages all compliance seamlessly in the background; whether you need multiple merchant accounts varies by acquirer/processor.

Register for 3-D Secure, including Verified by Visa, with your acquirer. Don’t do this until you know which payment gateway will be used and get their instructions if applicable.

Communicate with customers. Advise any upcoming changes will increase efficiency and security for everyone.

Why comply? With full compliance, merchants can expect better qualified interchange rates, increased approvals (avoid declines based on issuer risk averse algorithms), reduced PCI Compliance burden, and increased efficiency for both buyer and seller. The cost of non-compliance is hefty, including higher interchange rates, penalty fees, and risk of both issuer and cardholder chargebacks.

The same transaction can process at different rates as shown above, depending on which rules you follow. CenPOS Smart Rate Selector automates compliance to qualify transactions at the lowest rate possible. Which rates are on your merchant statement now?

Why should developers choose CenPOS for their integrated payment gateway? CenPOS has native modules for ERP, shopping cart, accounting and other software.

Increase profits faster

More efficient, quicker reconciliation

More secure- from Encrypted Virtual Keypad to elimination of credit card auth forms

More robust- Wire, ACH, check, Paypal, credit card and more; text and email payments supported. No 3rd party Electronic Invoice solution needed such as BillTrust; CenPOS invoice portal and automated collections included.

Where can I buy CenPOS or learn more? You’ve already found one of the top salespeople, Christine Speedy. All agreements are direct with CenPOS, no middle man.

DISCLAIMER: condensed and incomplete information! Information may be quickly outdated.

With the fast pace of changing rules, companies need a technology partner to automate compliance. Did you know?

CenPOS has a suite of solutions for companies just like yours, solving common problems and increasing profits virtually overnight.

For those not ready to give up paper, CenPOS creates a printable PCI Compliant credit card authorization form for every stored card.

CenPOS has ERP, ecommerce shopping cart, accounting and other plug-in modules available for quick and easy implementation.

I’ve been selling for CenPOS since day 1. Though I have other payment gateways available in my arsenal, nothing else compares for meeting business to business needs.

Christine Speedy, CenPOS authorized reseller, 954-942-0483 is based out of South Florida and NY. CenPOS is a merchant-centric, end-to-end payments engine that drives enterprise-class solutions for businesses, saving them time and money, while improving their customer engagement. CenPOS secure, cloud-based solution optimizes acceptance for all payment types across multiple channels without disrupting the merchant’s banking relationships.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.