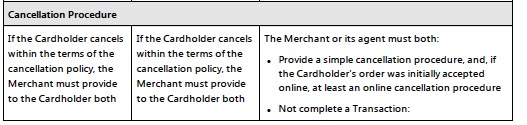

Do you hate it when you want to cancel a recurring billing service, but the business doesn’t let you cancel online and instead provided a phone number? Merchants offering SaaS or any recurring billing sign-up online, must allow customers to cancel online to comply with the Visa Stored Credential mandate.

Visa Product and Service Rules Table 5-20: Requirements for Prepayments and Transactions Using Stored Credentials, October 2018, pg 444.

What if a business does not allow you to cancel online? Report Visa violations here https://usa.visa.com/Forms/visa-rules.html. It says for in store only, but there is a check box for recurring transactions. The web site also says to contact your financial institution via the phone number on the back of the card.

The basis for the change is to enable customers more control over their purchasing, and stored card management. It makes sense if you can buy online 24/7, then you should be able to cancel online 24/7.

Rules for merchants to store cards and use stored cards changed dramatically in 2017, with enforcement beginning last year. Compliance is not automatic. Payment gateways manage most of the technical details, however, not all payment gateways are capable yet. Compliance is not optional and merchants are getting notices of violations subject to assessments and fines if not resolved. If your payment gateway or integrated solution does not support the needs to comply with the stored credential mandate, contact your acquirer, or credit card processor, to request a temporary waiver.

Call Christine Speedy, CenPOSGlobal Sales. 954-942-0483, 9-5 ET for all your recurring billing and stored credential payment gateway and virtual terminal needs. CenPOS is an integrated commerce technology platform driving innovative, omnichannel solutions tailored to meet a merchant’s market needs. Providing a single point of integration, the CenPOS platform combines payment, commerce and value-added functionality enabling merchants to transform their commerce experience, eliminate the need to manage complex integrations, reduce the burden of accepting payments and create deeper customer relationships.

MasterCard monitors the transaction data detail submitted by the acquirers, or merchant processors, to ensure the accuracy and integrity of the data. Data integrity reporting is accessible by acquirers and when problems are found, merchants are notified, typically with a short timeframe to correct the problem before non-compliance assessments and fines will be allocated.

Merchants often experience an increase in Data Integrity failures when not compliant with changing rules. For example, a MasterCard Data Integrity reporting as failing Edit 21, Recurring CoF Monitoring, refers to using a stored Credential On File for recurring billing. These are merchant initiated transactions on a fixed schedule for a fixed amount. Per MasterCard, all recurring payments are considered credential-on-file transactions.

“MasterCard requires POS entry mode= 10 (credential-on-file) to be sent for transactions identified as recurring. Please work with the POS vendor and these locations to correct the POS entry mode. If corrections are not completed, merchants are subject to non-compliance assessments and fines will be allocated.”

POS is an abbreviation for Point of Sale, even though recurring billing is not run via a traditional point of sale device. The payment gateway is critical to compliance and most likely is not sending the correct data, though it’s possible problems exist in other areas of the payment ecosystem, for example, with the acquirer. All US merchants are required to be compliant with stored credential rules that rolled out over 2017 to 2018. Some gateways now support the correct data set for recurring billing, but still lack support for Installment and Unscheduled. Payment gateways and solutions providers rarely advise merchants when they don’t have a solution, just when they have something new. Thus businesses may be in for a surprise with an urgent notice to correct a compliance violation.

Call Christine Speedy, CenPOSGlobal Sales. 954-942-0483, 9-5 ET for all your recurring billing and stored credential payment gateway and virtual terminal needs. CenPOS is an integrated commerce technology platform driving innovative, omnichannel solutions tailored to meet a merchant’s market needs. Providing a single point of integration, the CenPOS platform combines payment, commerce and value-added functionality enabling merchants to transform their commerce experience, eliminate the need to manage complex integrations, reduce the burden of accepting payments and create deeper customer relationships.

Recurring CoF monitoring is related to merchants using stored cards on file for recurring billing. Merchants are getting notices from acquirers about failing MasterCard Data Integrity reporting and, from what I’ve seen, only have two weeks to correct the issues.

The below merchant has been identified by the latest MasterCard Data Integrity reporting as failing Edit 21 – Recurring CoF Monitoring. Per MasterCard, all recurring payments are considered credential-on-file transactions. MasterCard requires POS entry mode= 10 (credential-on-file) to be sent for transactions identified as recurring. Please work with the POS vendor and these locations to correct the POS entry mode. If corrections are not completed, merchants are subject to non-compliance assessments and fines will be allocated.

Basically, a merchant must comply with rules about how a transaction is presented to the acquirer and the issuer for authorization. The payment gateway is largely in control of sending the correct data with each transaction. In the example violation notice, the merchant is not compliant with recurring payment rules which requires specific steps when storing a card for the first time and then for ongoing payments.

The 3Dmerchant.com blog has many articles about the Visa Stored Credential Mandate. Visa’s are the most stringent and by following them, merchants will also be compliant with MasterCard’s. The rules went into effect in October 2017, with enforcement delayed to May 2018. Despite some claims to the contrary on payment gateway web sites, the mere fact that a payment gateway can support the correct data set does not make a merchant compliant automatically. Merchants should read the rules on this web site, which includes links to the card brand rules.

Card brand rules (Visa, MasterCard etc) are constantly changing and many payment gateways have not kept pace with been given a notice, then don’t call your existing provider. The rules were announced in 2016 and went into effect for most businesses (some were earlier) in October 2017. If your vendor let this happen to you, it’s time to get advice from another source. Here’s a list of payment gateways compatibility status.

Call Christine Speedy, CenPOS Global Sales. 954-942-0483, 9-5 ET for all your stored credential payment gateway and virtual terminal needs. CenPOS is an integrated commerce technology platform driving innovative, omnichannel solutions tailored to meet a merchant’s market needs. Providing a single point of integration, the CenPOS platform combines payment, commerce and value-added functionality enabling merchants to transform their commerce experience, eliminate the need to manage complex integrations, reduce the burden of accepting payments and create deeper customer relationships.

Credit card authorization form 2019 templates are starting to pop up on the internet. The forms are never PCI compliant nor compliant with card network rules, plus the form might introduce malicious code into your network, leading to a future data breach. In this article learn about compliant credit card authorization form problems and solutions.

Merchants must replace traditional credit card authorization forms with other payment methods where the customer self-pays in 2019. The services are typically provided by a payment gateway, acquirer or software solutions provider. I recommend using an independent payment gateway for the checkout because if other changes are made, such and changing acquirer, it’s non-disruptive to customers and business processes.

Three solutions to replace traditional credit card authorization forms:

Hosted pay page is a third party hosted web page where buyer can enter all their payment information for immediate payment, and in some cases store it for future payments.

Pushing out a payment request via text or email includes link to a hosted prefilled pay page that can include an invoice number and amount due.

Electronic invoicing may be standalone or integrated and empowers buyers to pay online.

Per Visa, merchants are never allowed to ask for the security code in any written form. Merchants also cannot store the form with full card numbers nor store the security code after authorization. Traditional credit card authorization forms increase risk of fraud and identity theft and nobody likes them!

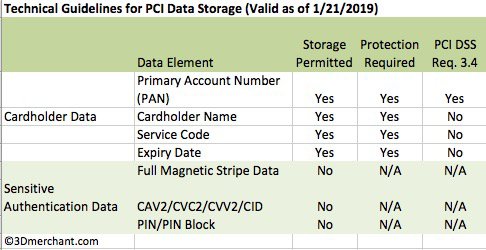

PCI Security Standards Council guidelines for storage of cardholder data.

Cardholder verification with 3-D Secure shifts fraud liability to the issuer, so instead of responding to chargebacks, merchants can prevent them from happening. This is far more powerful than using security code or address for cardholder verification, and eliminates the need for traditional credit card authorization forms. 3-D Secure is a set of global security standards, for example, Verified by Visa.

Phone order payments risk identity theft:

Phone orders expose card data to employees.

Employees often write the cardholder information down on paper first to avoid making a mistake that requires them asking for the information again.

While less than 15% of data breaches occur from insider threats, trusted employees do steal data for financial, espionage, and grudge reasons.

It costs more to process the card both in actual labor and in card acceptance fees because it’s impossible to qualify for the lowest card not present rates possible on manually key-entered transactions.

Fax order payments risk identity theft:

All of the phone order risks apply, plus new risks for fax.

Digital faxes have memory where data can be stored, risking theft during use and after disposal of hardware.

Depending on access to the hardware or software, many people might have access to faxed forms, including evening cleaning service personnel.

Merchants cannot ask for security code on the form, yet it’s required for card not present transactions.

The card number must be masked after use if being stored

Storing the form has no value because if proper card not present rules are followed, there’s no need for it to defend chargebacks.

Cloud digital credit card authorization forms may not be PCI compliant:

The rise in digital credit card authorization forms is downright scary, because despite claims by sellers, merchant implementation of them is often not PCI Compliant. Here’s a few reasons why:

Neither merchants nor third parties can store the security code after authorization.

Neither merchants nor third parties can store the card number unmasked after authorization.

Merchants will be hard pressed to prove PCI Compliance in the event of a data breach. Who had access to the forms and when? How is the server wiped of the data? What about back up servers?

What’s the point of getting a signed form if you can’t save it?

If the service offers an authorization to verify cardholder, but the merchant then types card number into another system with no connection to the initial verification, all subsequent transactions are in violation of rules for storing and using stored cards thus are open to issuer chargeback risk.

Benefits of compliant solution:

Reduced merchant fees for some cards (3-D Secure cardholder authentication such as Verified by Visa must be enabled.) Increased approvals with cardholder authentication. Mitigate chargeback risk – with 3-D Secure cardholder authentication, fraud liability shifts to issuer. More convenient for buyers- 24/7 payments on their schedule, not yours. Buyers are in control of choosing to store payment methods

How can merchants get 3-D Secure? Contact us for the latest instructions or call your acquirer aka merchant services provider.

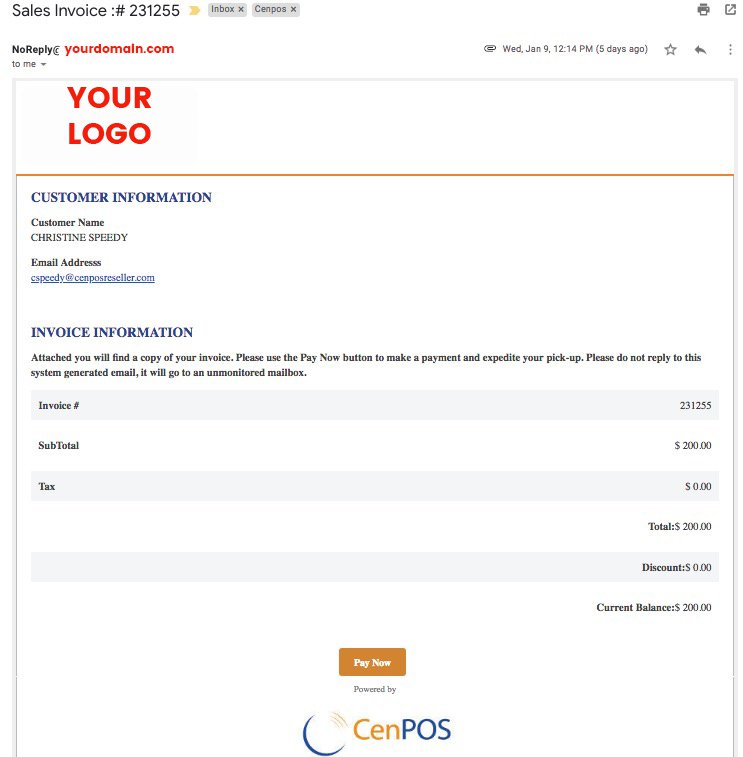

Microsoft Dynamics AX and D365 users need a more customized invoice and sales receipt subject and body than they have with their current solution. The CenPOS F&O accounts receivable module includes the 3 most common requests users ask for.

Create a custom subject and automatically insert the invoice number. For example, Sales Invoice # 231255.

Create a custom body plus automatically insert subtotal, invoice #, sales tax, discount, total invoice etc and a click to pay link.

Attach a PDF invoice

Invoices can be delivered via multiple methods and customers can pay via ACH, wire, credit card and other payment types directly from the email or text; customers can also login to a portal to view and pay multiple invoices. This increases efficiency for both parties and is proven to reduce DSO Because CenPOS is both the invoicing solution and a PCI Level 1 Service Provider, merchants can eliminate Red Maple Advanced Credit Cards, Billtrust and similar other third party solutions.

The sales receipt works pretty much the same way, with receipts automatically delivered via the customers preferred communication method.

The CenPOS F&O module is quick and easy to implement. All these features and more are available standalone or integrated. Integrators, developers and Dynamics users can contact Christine Speedy at 954-942-0483 for the module.

Call Christine Speedy, CenPOS Global Sales, PCI Council QIR certified, for the CenPOS Dynamics AX and D365 modules to make your business more profitable, efficient and secure. 954-942-0483, 9-5 ET.

CenPOS is an integrated commerce technology platform driving

innovative, omnichannel solutions tailored to meet a merchant’s market

needs. Providing a single point of integration, the CenPOS platform

combines payment, commerce and value-added functionality enabling

merchants to transform their commerce experience, eliminate the need to

manage complex integrations, reduce the burden of accepting payments and

create deeper customer relationships.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.