Replacing ICVerify or other legacy software for batch credit card processing? Whether you’re in the cloud, or headed there, methods of payment processing have changed to meet current and future requirements for PCI Compliance and fraud prevention. For service providers, including non-profit mail processing, payment gateway selection impacts efficiency, merchant fees, and even client PCI Compliance burden.

The first way efficiency can be increased is the batch upload process. It’s basically the same for credit card processing and check processing. Here’s comparisons for payment gateway methodology for batch upload service:

CenPOS Batch Processing File Upload

- Save file to configurable directory (listening folder)

CenPOS Batch Processing Response File Retrieval

- Retrieve one or multiple files from configurable directory (response folder)

Authorize.net, Payeezy (First Data) and similar Batch Processing File Upload

- Log in to your Merchant Interface at https://account.authorize.net or other

- Click Upload Transactions.

- Click Upload New Transaction File.

- Click Browse.

- Locate from your system the file that you want to upload.

- Click Upload File.

Authorize.net, Payeezy (First Data)and similar Batch Processing Response File Retrieval

- Log into the Merchant Interface at https://account.authorize.net or other

- Click Tools from the main toolbar.

- Click Upload Transactions.

- Click View Status of Uploaded Transaction Files.

- Select the desired uploaded transaction file from the Select Upload File drop-down list.

- Click Submit.

CenPOS increases efficiency to upload and retrieve responses, reduces friction with no login required, and also supports multi-merchant login, enabling users to toggle between accounts, creating efficiency for both the service provider and the merchant.

| More BATCH UPLOAD differences | authorize.net | CenPOS |

| Custom fields (share across channels) | No | Yes |

| Reporting | 2 years | Indefinite |

| Telephone support | no | yes 24/7 |

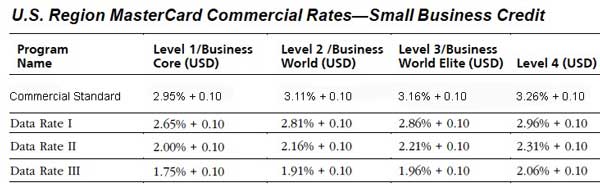

Merchant fees are impacted when a transaction does not qualify at the lowest interchange rate possible. For example, business to business companies must submit level III data to qualify for related rates, which are often 90 basis points (0.90%) lower than without. The payment gateway must be certified for level III to each acquirer supported. Only a few payment gateways are level III certified, and even fewer of those offer an acceptable batch upload solution.

PCI Compliance burden is reduced with tokenization, outsourced payment processing, reduced vendors and reporting. The latter is critically important for forensic audits, as well as financial. The average gateway only saves data for two years, and has limited data retrieval capabilities. CenPOS audit reports cover every touch to the platform- who, what, when, and more, with records available for a minimum of 7 years to match IRS requirements, reducing the cost of on-site and remote audits.

To learn more about batch credit card processing, replacing ICVerify, and cloud payment differentiators, Contact Christine Speedy for a free consultation for all your omnichannel global payment needs.