American Express merchant services deposits are now faster. As of April 2021, merchants see deposits the next business day after the transactions are submitted Monday through Friday. As of October 2020, merchants are receiving separate payment deposits for Friday, Saturday and Sunday on Monday to help simplify payment reconciliation.

American Express receipts for small businesses now appear on merchant statements with other credit cards, depending on when the merchant account opened. Older merchant accounts that did not sign up for the new program, merchants that prefer separate, and those that do not meet the maximum processing limits receive separate statements from American Express instead of their acquirer.

Call Christine Speedy, PCI Council QIR certified, for all your credit card processing questions and services. 954-942-0483, 9-5 ET.

New interactive online resource to help card issuers, merchants and solution providers optimise the EMV® 3DS payment authentication experience for e-commerce consumers.

16 August 2021 – Global technical body EMVCo has published EMV® 3-D Secure (EMV 3DS) UI/UX Design Guidelines to help card issuers, banks, merchants and solution providers optimise the EMV 3DS payment authentication experience for e-commerce consumers. The guidelines are publicly available on the EMVCo website in an easy-to-use interactive format. In e-commerce purchases where EMV 3DS solutions are used, EMV 3DS user interface (UI) and user experience (UX) design refers to the look and feel of the screen that consumers interact with on their device during authentication with their card issuer. This includes how visual components (e.g., logo, colour, iconography, etc.) are displayed in various device layouts, and how information is presented and communicated to guide them through the steps for verifying that they are the legitimate cardholder. According to an EMVCo-commissioned global market research study1, consistent, familiar and efficient EMV 3DS UI/UX design is key to instilling consumer trust in the authentication process and optimising the checkout experience during shopping. The new guidelines are designed specifically to help card issuers, merchants and EMV 3DS solution providers achieve this objective and deploy user interfaces for EMV 3DS authentication that support a secure and seamless e-commerce checkout experience. “Authenticating the individual making the payment continues to be key in the fight against e-commerce fraud. The EMV 3DS UI/UX Guidelines support the consistent implementation of EMV 3DS for fraud prevention to deliver an efficient and trusted e-commerce consumer experience, which benefits the entire payment ecosystem,” said Robin Trickel, EMVCo Executive Committee Chair. The EMV 3DS UI/UX Guidelines are supplemental to the EMV 3-D Secure User Interface Templates, Requirements, and Guidelines chapter in the EMV 3DS Protocol and Core Functions Specification. 1 Methodology: Qualitative and quantitative usability study conducted in 2019-2020. Featured surveys with 650+ participants in UK, Brazil, China, France, Singapore and the U.S.

To learn more, view the EMV Insights post: Optimising the EMV 3DS Payment Experience: UI/UX Design Guidelines. About EMV 3DS EMV 3DS is a fraud prevention technology that enables consumer authentication, without adding unnecessary friction to the payment process that often leads to abandoned purchases. The EMV 3DS Specification provides a common set of requirements product providers can use to integrate this technology into their solutions to support seamless and secure e-commerce payments. View the EMV 3DS Press Kit to learn more.

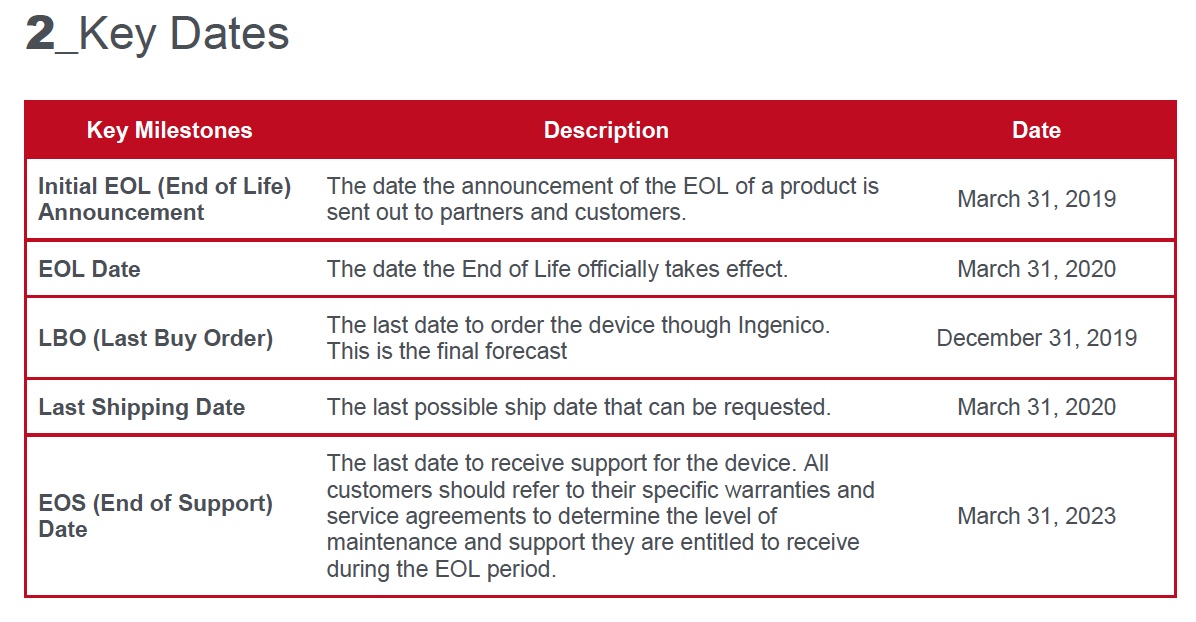

Ingenico announced end of life for the ISC 250 with PCI PTS v3 and v4 in March of 2019. This has not stopped companies from selling them, however, due to the PCI PTS expiration in April 2021, merchants who use them would not be able to prove PCI compliance in the event of a data breach.

Did you know terminals have their own Payment Card Industry or PCI certification? The standards are part of the overall merchant requirements to maintain the security of cardholder data. Those rules change over time and a bunch of Ingenico equipment recently expired, including the popular ISC250 lane terminal.

Ingenico issued end of life notifications on their PCI PTS 3 range of payment devices in compliance with the PCI Security Standards Council PCI 3 expiration date of April 30, 2020, which was extended to April 30, 2021 due to Covid. Often merchants will get notifications like this from their acquirer on their merchant statement.

Which Ingenico terminals are impacted?

iSC Touch 480 PCI-PTS v3/4 model

iSC Touch 250 PCI-PTS v3/4 model

iPP320 PCI-PTS v4

iPP350 PCI-PTS v4

This list does not include all devices! Merchants should check with their providers especially if using a non-EMV device or if you were an early EMV chip adopter.

Ingenico isc250

What does End of Life mean?

(PCI) PIN Transaction Security (PTS) v3 expires April 30, 2021.

(PCI) PIN Transaction Security (PTS) v4 expires April 30, 2023.

PCI PTS v5 expires April 30, 2026.

Are merchants PCI Compliant if they continue to use PCI 3 terminals after April 2021? The PCI Council urges but does not mandate merchants use approved PTS devices in their payment environments. However, in our experience, between payment brand and acquirer requirements, merchants generally need to use only approved PTS devices or risk getting shut down. Research expiration dates of terminals on the PCI Council web site. I’d be concerned about liability and the ability to prove PCI compliance, especially in the event of a data breach. If security vulnerabilities or exploits are identified by processors after April 2021, and you’re using the terminals, who’s to say when or even if a solution could be found to fix it?

How disruptive would it be for your business to have to shut down using them and get another solution? There are always people who procrastinate making changes. And when something goes wrong, phone calls to processors explode, so change is usually not as swift as you’d like.

Note, only employees and PCI QIR certified individuals can install or touch your credit card terminals. Terminals are one of the most important factors determining rates you pay and chargeback risk. Why? Call now to learn more. This is the perfect time for an external account review by a payments expert.

TIP for Christine Speedy Ingenico ISC250 customers: If you were an early adopter and had your terminals deployed prior to the EMV chip liability shift in October 2015, there’s no need to check part numbers; They need to be replaced. Please contact me directly to consult on replacement options.

Call Christine Speedy , PCI QIR certified, for new PCI 5 terminals, technology review and or merchant account review to maximize profits and improve your customer experience. 954-942-0483, 9-5 ET

Looking for a D365 F&O credit card processing solution? Very few check all the boxes. There are different nuances to each and a big consideration should also be the level of customization that is needed. How much work is needed to get the module live and continually updated?

Our D365 F&O credit card processing solution minimizes the need for customization and is light to implement, creating opportunities to save tons of money on consulting, development, and updates. Users receive a deployable package and continual updates to work with all D365 updates.

Built based on years of experience with ERP payment processing and especially the needs of B2B manufacturers and distributors, including omnichannel, here’s a few examples:

Supports RETAIL, MOTO and ecommerce. Yes, that’s retail transactions within F&O, not D365 Retail.

Retail accepts EMV chip, checks and cash.

Retail Level 3 processing reduces B2B costs.

Prepay on sales authorization.

Split payments among multiple payment methods.

Stored card and ACH info- tokenized, never visible.

Automated daily batching.

Automated journal updates.

Payment object resides outside of the ERP environment for reduced PCI scope.

Optional validated P2PE.

Automated compliance with authorization and stored credential rules.

Optimization for least cost processing any given transaction.

Compliant with rental and loaner special processing requirements.

Call Christine Speedy, PCI Council QIR certified, for all your Microsoft Dynamics AX and D365 payment processing needs from ACH to credit cards and more. Get a new merchant accountor keep your existing. 954-942-0483, 9-5 ET.

Massachusetts joins other states that still have a credit card surcharge ban on the books, with a bill to repeal. Since the 2017 US Supreme Court ruling regarding the NY case that it regulates speech, every state with a surcharge has repealed, introduced a bill to repeal, has already lost a case in court, or is in the process thereof. This is especially good news for B2B companies.

Massachusetts Senate and House are both in agreement with the February 2021 bill and it is now in committee with status “arrived” as of April 13, 2021.

Colorado also has a bill pending. The U.S. District Court for the District of Kansas approved a part of plaintiff’s motion for summary judgment in an action concerning whether a state statute that bans credit card surcharges violates the First Amendment.

Many in the legal and credit card processing community support B2B merchants can surcharge in all states and that the regulations only apply to consumers. Numerous court cases have resulted in positive results for plaintiffs.

Does your company want to surcharge? Call Christine Speedy right now at 954-942-0483, 9-5 ET for a compliant solution. Please share your surcharge insights for others and ask any questions below. The information herein is based upon public information available at the time written and may change.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.