- Lack of brute force attack tools. These help prevent bots from testing thousands or millions of cards on your checkout form. The merchant is liable for all of the attempted transaction fees on the payment gateway and on the acquiring. A simple first line of defense is adding recaptcha. See Visa best practices to prevent brute force attacks. https://usa.visa.com/support/merchant/library/visa-merchant-business-news-digest.html.

- Non-compliance with Visa Stored Credential Mandate, effective October 14, 2017? I’ve written extensively on this, for example here’s a B2B steps to compliance article. There are multiple elements, and many payment gateways do not yet have solutions, especially for ‘Unscheduled credential on file’. Do you have a checkbox in the sequence of checkout opting in to terms? https://usa.visa.com/dam/VCOM/global/support-legal/documents/stored-credential-transaction-framework-vbs-10-may-17.pdf.

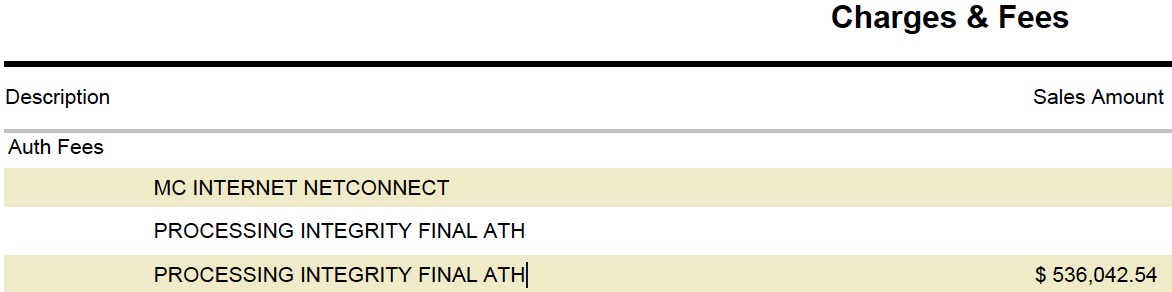

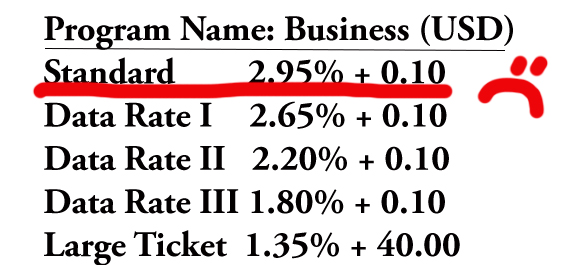

- Invalid authorizations. This is the most costly as it can lead to consumer generated chargeback, issuer chargeback, non-qualified interchange rates and penalty fees. Here’s a story about the new .25% MasterCard integrity fee. Do you have Standard/STD, EIRF, or Data Rate I on your merchant statement under interchange fees? Then you have an authorization problem.

- Cardholder authentication limitations. The security code has historically not been enough evidence to win customer disputes about unauthorized charges. With 3-D secure, fraud liability shifts to the issuer. Effective April 2019 based on region and industry, Visa mandates many merchants use Visa 3D Secure 2.0. Reference Table 5-18: Acquirer Support of Verified by Visa, Visa Public Rules.

The solution to all of the above is replacing outdated payment gateway technology with new technology that will help automate compliance with card network rules, while reducing PCI Compliance burden.

Why comply? Here’s an example of the cost difference between valid and invalid authorization.

Resources and documentation /blog/merchant-bulletins-downloads – bookmark it!. Join Christine Speedy’s email list.

DISCLAIMER: condensed and incomplete information! Information may be quickly outdated.

Need a solution? Call Christine Speedy, 954-942-0483, 9-5 ET, CenPOS authorized global reseller based out of South Florida and New York. CenPOS is an integrated commerce technology platform driving innovative, omnichannel solutions tailored to meet a merchant’s market needs. Providing a single point of integration, the CenPOS platform combines payment, commerce and value-added functionality enabling merchants to transform their commerce experience, eliminate the need to manage complex integrations, reduce the burden of accepting payments and create deeper customer relationships.