Winter Storm Jonas is a reminder of the importance for business to business companies to accept payments online. What if you have a desktop terminal, but staff is working from home? How can accounts receivable be reached for call in or fax payments? Cash flow and efficiency will improve with 24/7 online payments. To accept payments online via a self-serve 24/7 online payment form, a payment gateway is required to secure the transaction. The most popular non-integrated methods:

To accept payments online via a self-serve 24/7 online payment form, a payment gateway is required to secure the transaction. The most popular non-integrated methods:

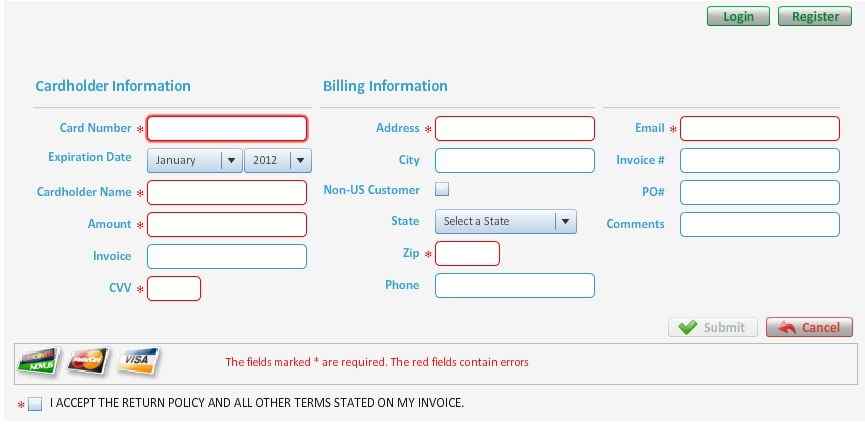

- Hosted pay page – merchant provides customers an email or web site link to make payments on the payment gateway hosted web page. Click here for hosted pay page example.

- Embedded payment object– the buyer stays on the merchant web site, with the gateway html code embedded as an iframe.

Online Payments FAQ

What is the rate? There are two service types: Payment gateway or bundled gateway with merchant account. For flexibility to change merchant accounts, which most businesses will do every few years, keep your gateway separate to minimize business disruption. When the merchant account changes, there’s no programming needed. Just update the gateway settings with the new merchant account information. Never, ever choose a payment gateway by comparing the cost per transaction. Instead, measure the net transaction cost, including gateway fees, for card types accepted. (Click here for online payments example of authorize.net vs CenPOS for business to business.) B2B companies need a gateway solution that supports level III processing and will help qualify transactions for the lowest rate.

How long does it take to get started? Usually 2-5 days after the decision has been made, from gateway sign up to accepting payments. The actual implementation time is minimal.

How do I know when someone makes a payment? An email is automatically sent with details. TIP: Create an email alias to a distribution list. For example, epay@mydomain.com.

Can my invoices be automatically marked as paid in my accounting software? With an integration, yes. Depending on your software, and the gateway, there may be a module available for quick and easy implementation.

Where can I view transaction reports? By logging in to the virtual terminal via a secure web browser, or in some cases, via mobile app.

Can customers save their credit card information? With most gateways, yes.

Is it PCI Compliant? All the major US payment gateways are PCI Compliant. Accepting payments online can improve PCI Compliance for merchants, as risky practices like credit card authorization forms are abolished.

Can customers pay with an echeck (ACH)? It depends on the gateway.