What’s the most important EMV implementation criteria for business to business retail? Supporting level III data, which increases profit margins by qualifying credit card transactions for the lowest interchange rates possible. With proper terminal selection, businesses can quickly offset the cost of compliance for chip card acceptance, and protect long-term profit margins.

“The most recommended terminals in the US, including all the First Data FD series, Verifone VX series, and Ingenico iCT series terminals, do not meet critical business to business needs to protect profit margins, ” said Christine Speedy, a global CenPOS Authorized Reseller.

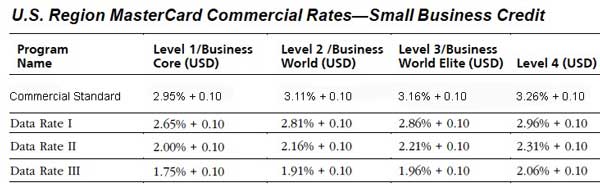

Interchange is the primary component of credit card processing fees, typically accounting for over 95% of fees. For business to business (B2B), including building supply and HVAC, many customers use corporate, business and purchasing cards. By qualifying these cards for level III interchange rates, B2B merchants can boost margins significantly. For example, the MasterCard interchange rate can drop from 2.65% to 1.80%, for transactions under $7500, and even more for larger transactions.

What’s needed to qualify for level III rates? The US EMV ecosystem at a minimum requires a web-based payment gateway that has certified an EMV terminal with level III processing to a specific acquirer. That’s because the extra data needed for the transaction is too cumbersome for a countertop terminal, but can be easily managed with a cloud solution. For example, CenPOS has certified the Verifone MX915 to First Data, Chase Paymentech and Tsys, the latter which enables use with most processors. Merchants can use CenPOS via a web browser virtually instantly or an integrated application.

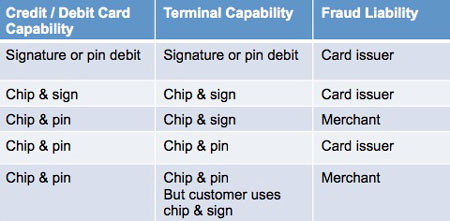

While there is no mandate for chip card acceptance, effective October 1, the party that does not support EMV (short for Europay, MasterCard, Visa) chip card acceptance is liable for counterfeit card, and sometimes lost or stolen card transactions. Additionally, non-EMV compliance fees have already been announced by at least one provider starting January 1, 2016.

About CenPOS

CenPOS is a merchant-centric, end-to-end payments engine that drives enterprise-class solutions for businesses, saving them time and money, while improving their customer engagement. CenPOS’ secure, cloud-based solution optimizes acceptance for all payment types across multiple channels without disrupting the merchant’s banking relationships.

For global sales and integrations, contact authorized reseller Christine Speedy 954-942-0483.