What’s the best EMV payment technology for business to business (B2B) merchants? Once the requirements are defined for non-EDI payments, the options are limited. Whether card not present only, or a mix of retail, phone, and ecommerce, B2B payments are different.

B2B Credit Card Payment Minimum Requirements.

- Tokenization to store credit card, and possibly check and wire data

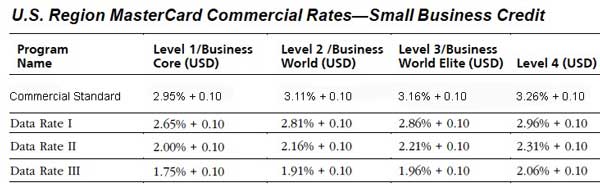

- Level 3 processing (significantly reduces merchant fees through lower qualified interchange rates)

- Payment optimization to qualify transactions properly. For example, if merchant does a pre-authorization, and captures at a later date, certain rules need to be met to avoid higher non-qualified interchange rates.

- 24/7 payment options for customers to serve multi-time zone and increase security

EMV Terminals for B2B.

There are no desktop or countertop terminals that support level III processing, and that won’t change. These terminals are programmed with the acquirer instructions via download, and less frequently, may be connected to Point of Sale (POS) software.

To meet the minimum B2B requirements, a payment gateway is required. Merchants process transactions by accessing a virtual terminal via a secure web page, or with an integrated software solution. The gateway must certify level III processing for each card brand, and EMV, and the specific terminal, for each acquirer.

For example, CenPOS has certified the Verifone MX915 to TSYS, with P2P encryption, level III processing. Most acquirers and banks support TSYS as a way to connect to their platfor; for example, First Data, Chase Paymentech, and Bank of America Merchant Services. To date, no other gateway has certified level 3 processing for retail and EMV. The difference for distributors is huge; it’s not uncommon to reduce merchant fees an average of 30%.

Pending Certifications

Exercise caution on claims of pending certifications, if the solutions provider:

- Doesn’t have any certifications to date, after a year or more to prepare.

- Has never had level III processing for retail certification

- Does not offer a way to automate interchange management in a mixed retail & card not present environment, or for card not present only