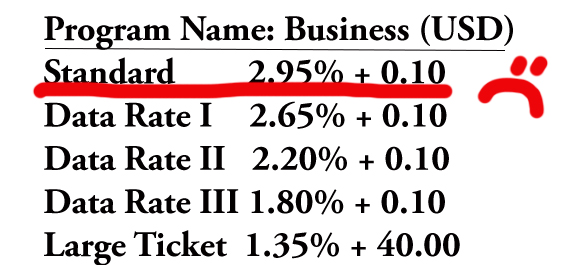

Level 3 processing requires payment solutions that can both send level data and dynamically optimize transactions to qualify for level 3 rates. Learn the secrets to higher profits right now. Were you told your last solution would fix your problems so you’d qualify properly? Have you been told with more training you could fix the problems to hit level 3? Hogwash! It’s not your fault, you just didn’t have an insider perspective until now.

Many payment gateways can send level 3 data, but the requirements to qualify for level III interchange rates are much more complicated than that. Do you perform preauthorizations? You know what happens when the preauth expires? Or when the final settlement is not the same as the preauthorization? These are just two of many reason merchants fail to qualify for level 3.

New rules for storing cards and using stored cards can also impact profits. Hint: If you haven’t made big changes to how you do this since October 2017, you’ve got a problem. Failure to comply with any rules negates rate qualification. If issuers are not sophisticated enough to catch all the rule breakers now, it’s only a matter of time. In the future, cardholders will be able to login to their bank and view all the companies that are storing their cards. So if you haven’t made the changes needed per new stored card requirements, including the new Unscheduled Credential On File (UCOF) transaction indicator, that creates a problem for the long term goals in financial industry. Compliance enforcement can include penalties and assessments.

I’ve seen demo’s, heard sales pitches, and read the documentation on many payment gateways and virtual terminals. It’s not what’s there, but what’s not there that is most revealing. Before choosing a level 3 processing solution, get a demo. If you’ll be using a virtual terminal, use that for the demo. If you’ll be using an integrated solution, view the integrated solution demo.

The demo:

- Store a regular card and business card. What methods are used to capture the initial card data? Then charge each card. Note the steps for each.

- How does the solution manage reversals on preauthorizations?

- What’s the process to identify and renew an expired authorization?

- How can buyer complete a transaction with 3-D Secure?

- Pull report to retrieve transaction.

- Pull report with level 3 data.

- Ask if the gateway supports Recurring, Installment, or UCOF depending on your needs; virtually all support Recurring, but not the others.

Note how much of the process is automated, how much relies on people making decisions, and if any items are not available. Take screenshots. On a Mac it’s command + shift+ 4.

Want a payments expert as a silent observer? Ask me to sit in on the call for unbiased feedback.

Call Christine Speedy, PCI Council QIR certified, for simple solutions to complex payment transaction problems, 954-942-0483, 9-5 ET. CenPOS authorized reseller based out of South Florida and NY. CenPOS is an integrated commerce technology platform driving innovative, omnichannel solutions tailored to meet a merchant’s market needs. Providing a single point of integration, the CenPOS platform combines payment, commerce and value-added functionality enabling merchants to transform their commerce experience, eliminate the need to manage complex integrations, reduce the burden of accepting payments and create deeper customer relationships.

Did you like this article?

Credit card fraud is still rampant in the US, even after US EMV liability shift convinced many merchants to purchase terminals to support chip cards. Marine, auto, and other high value parts dealers have long had a problem mitigating fraud risk with local and international parts.

Credit card fraud is still rampant in the US, even after US EMV liability shift convinced many merchants to purchase terminals to support chip cards. Marine, auto, and other high value parts dealers have long had a problem mitigating fraud risk with local and international parts.