Looking for solutions to fix CAPK errors on credit card terminals? In 2016, 3D Merchant blog explained about CAPK expired error messages on VeriFone EMV terminals and how to fix them. With credit card terminal lifespans of about 5 years, primarily due to security enhancements, the answers are different in 2022. Computers cannot be upgraded at some point and neither can credit card terminals.

The old article referenced the VeriFone EMV Vx520, FD55, Vx510, Vx570, among other terminals. A later blog post explained Verifone PCI 3 End of Life Terminals, which includes those and others. Merchants using the related desktop terminals, which typically require a manual download from the merchant acquirer to update, are unlikely able to get new updates due to the end of life process.

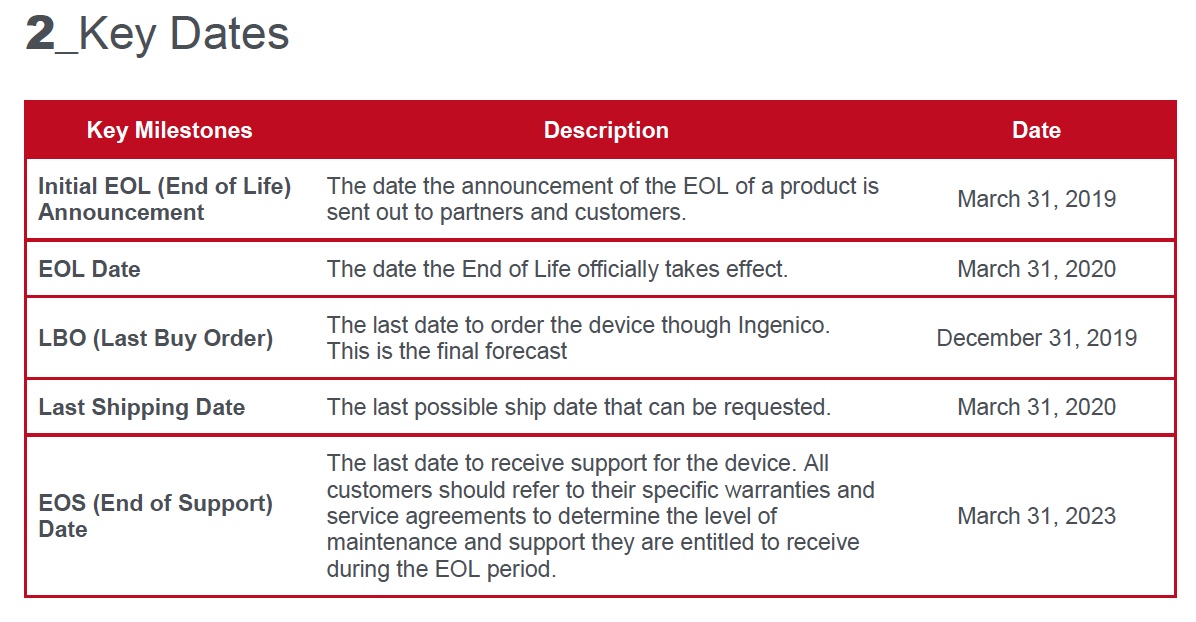

Previously Visa extended the EMV Certification Authority Public Keys (CAPK) key’s expiration date from 12/31/2015 to 2022, which required a terminal software update. Chip cards contain the issuers private keys which need to be verified by the card issuer’s public keys during online authorization requests. The keys come from the Certification Authority Public Keys (CAPK), and they expire periodically. Card readers reject transactions (decline) when an incorrect or expired CAPK is used. When a terminal reaches a certain point at end of life, they can’t be updated and the CAPK error is just another symptom of the current problem: it’s time to replace the credit card terminal.

CURRENT RECOMMENDATIONS:

- If you want to keep your current acquirer, and are interested in exploring technology solutions to enhance business operations, security and your customer experience, contact 3D Merchant Services for cloud technology solutions and compatible terminals. If your acquirer, refers you to 3D Merchant Services to solve your CAPK problem, this is how it will be done- equipment and processes WILL change. For 3D Merchant clients, the benefits far outweigh the cost to replace.

- If you want to keep your current acquirer and keep your equipment, only your current acquirer can help you resolve CAPK issue, if feasible. If you do not know how to reach your acquirer, a phone number is provided on your merchant statement.

How to identify if terminal is end of life?

- If it’s more than 5 years old, it almost certainly is. Look for date on the terminal.

- Look for PCI PTS version on the terminal.

- Call your acquirer.

- If your terminal uses PCI PTS, which is rquired certification for devices that accept pin code entry, 3.x (expired now) or 4.x (expires 2023), the time to plan for their replacement is NOW. Do not wait. The sources below are not that great because PCI web site now says to refer to manufacturers for research and limits which are listed on their web site.

- Google your “terminal name specifications”. A PDF spec sheet will have the PCI PTS version or their might be a sticker on the terminal with a date and or P

- Search for devices here on the Official PCI Security Standards web site https://www.pcisecuritystandards.org/assessors_and_solutions/pin_transaction_devices?agree=true

- On manufacturer web sites, look up the terminal security specifications. For example, this shows PCI PTS 4.x approved for the MX 915 currently for sale. https://www.verifone.com/en/us/devices/multilane/mx-915. PCI PTS 4.x expires in April 2023.

COVID ALERT: Due to supply chain problems, terminals are nationally in short supply for all manufacturers. 3D Merchant Services offers equipment sales only to customers. All terminals ship direct from certified facilities and are billed by the recommended solutions provider.

Call Christine Speedy, 3D Merchant Services owner and Authorized Reseller. Call for simple solutions to payment transaction problems. 954-942-0483, 9-5 ET.